1 month ago

21

1 month ago

21

Michael Saylor wants to make one thing very clear: Strategy is not dumping its Bitcoin. Not now. Not in any scenario that matters.

The executive chairman of Strategy, the company formerly known as MicroStrategy, responded to growing speculation that the firm might be forced to sell portions of its massive Bitcoin treasury to cover financial obligations. His answer was essentially: sure, we might sell a coin or two, but we’d be buying 10 to 20 more for every one that leaves.

The math behind the messaging

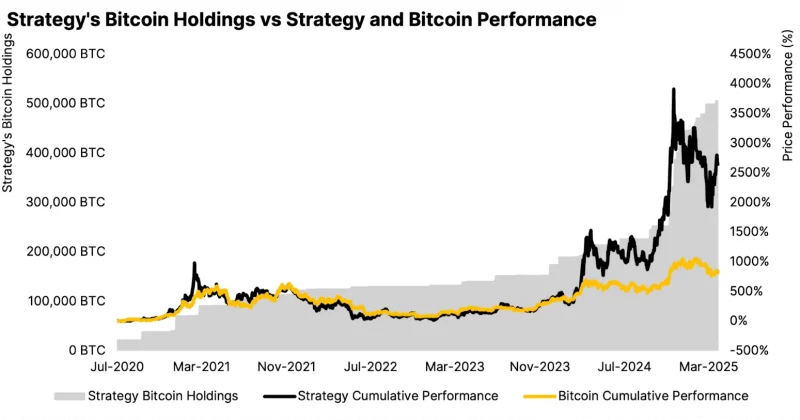

The company now holds 818,334 BTC, acquired at an average price of roughly $75,537 per coin. The company reported a staggering $12.54 billion net loss in Q1 2026, a figure that immediately raised eyebrows about whether the firm could sustain its current trajectory without liquidating some of its holdings.

Strategy carries approximately $1.5 billion in annual dividend obligations. Saylor’s answer is that Strategy funds its operations and Bitcoin acquisitions through a combination of equity issuances and debt instruments.

The key phrase in Saylor’s framework is “net seller.” He’s not categorically ruling out any Bitcoin sales ever. He’s saying that any disposal would be strategically paired with purchases that dramatically outweigh whatever was sold. In his words, for every one Bitcoin sold, the company would acquire 10 to 20 more.

Pushing back on the Ponzi narrative

Gold bug and persistent crypto skeptic Peter Schiff has been vocal about what he characterizes as a Ponzi-like structure at Strategy. The argument goes something like this: the company issues stock and debt to buy Bitcoin, Bitcoin’s price appreciation makes the stock more valuable, which allows more stock and debt issuance, which funds more Bitcoin purchases.

Saylor dismissed those claims directly. His position is that Bitcoin serves as Strategy’s primary treasury asset, and the equity and debt mechanisms are standard corporate finance tools being applied to an unconventional asset class.

The company isn’t losing money from operations in the traditional sense. It’s losing money because accounting rules require marking its Bitcoin holdings to market value.

Some analysts have described Strategy’s approach as a “never-ending cycle” of buying and selling Bitcoin to fund operations. The suggestion is that if Bitcoin rallies by around 30%, the company could comfortably sell small portions of its treasury to cover obligations while still adding to its overall position.

What this means for investors

For anyone holding Strategy stock, or considering it, Saylor’s comments are designed to address the single biggest existential question about the company: is there a scenario where Strategy becomes a forced seller of Bitcoin?

Senator Bernie Moreno recently announced the upcoming markup of the Clarity Act, legislation aimed at creating a more defined regulatory framework for stablecoins. While that bill targets stablecoin yields rather than Bitcoin directly, any regulatory clarity in the crypto space tends to ripple outward.

With $1.5 billion in annual dividends to cover and a balance sheet that swings by billions based on Bitcoin’s daily price action, institutional investors watching this space should pay attention to the spread between Strategy’s cost basis of $75,537 per coin and Bitcoin’s market price, because that spread is the only thing keeping the entire model solvent.

Disclosure: This article was edited by Editorial Team. For more information on how we create and review content, see our Editorial Policy.

English (US) ·

English (US) ·