6 hours ago

3

6 hours ago

3

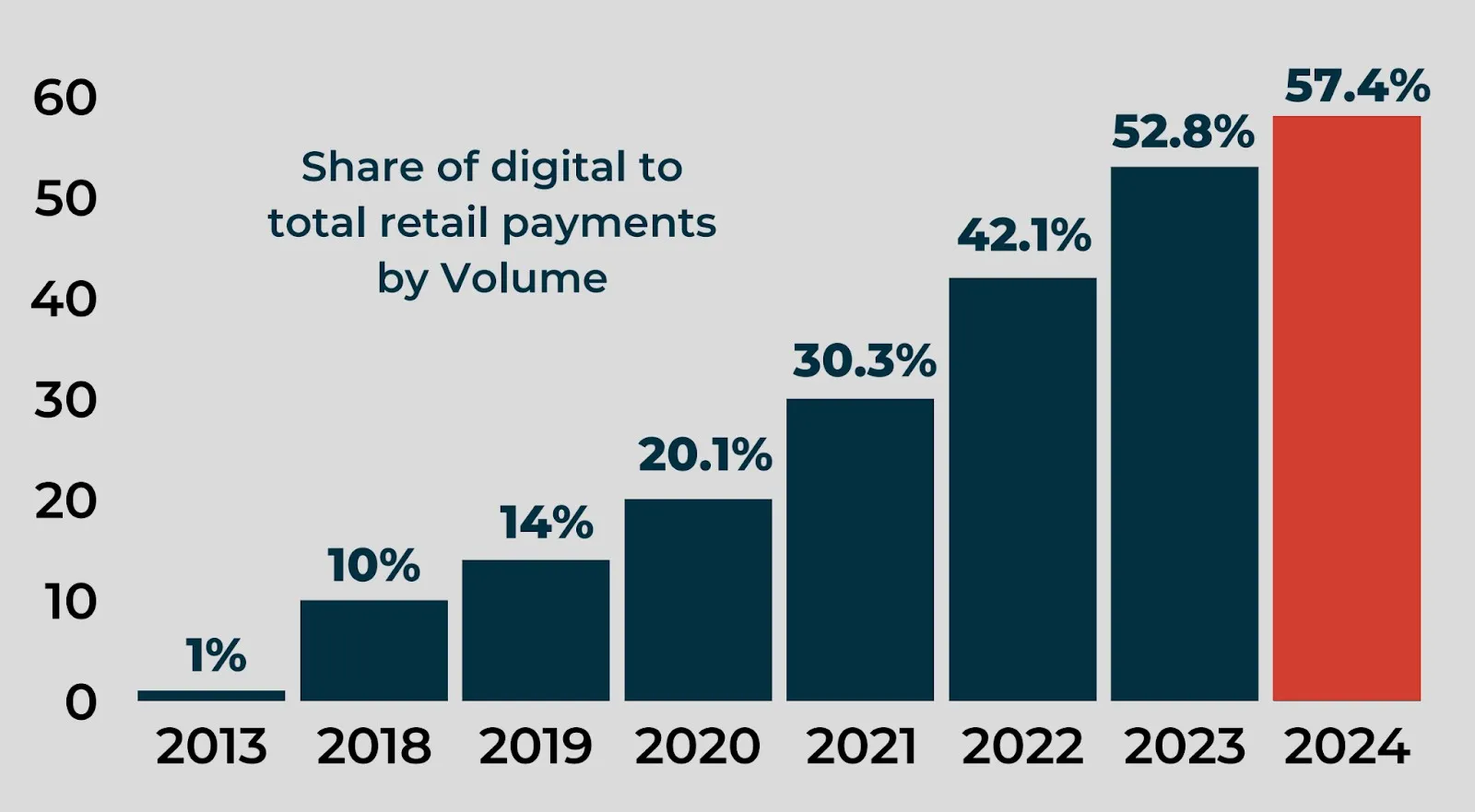

Digital payments have overtaken traditional cash-based transactions in the Philippines, with digital methods now accounting for 57.4% of total monthly retail payment volume and 59% of overall transaction value in 2024. This is according to the Philippine central bank, Bangko Sentral ng Pilipinas (BSP)’s 2024 report on the status of digital payments in the Philippines, which tracks the country’s shift toward electronic finance.

The latest data marks a 4.6% point increase from the previous year’s 52.8%. The numbers exceed the national target of 52–54% set under the Philippine Development Plan 2023–2028.

The central bank said this reflects a broad transformation in how Filipinos pay and manage money. “These figures reflect the continued shift toward digital channels and the growing trust of Filipinos in using digital financial services,” Eli Remolona, Jr., BSP Governor, said.

Source: BSP

Source: BSPMerchant, P2P, and B2B transactions lead growth

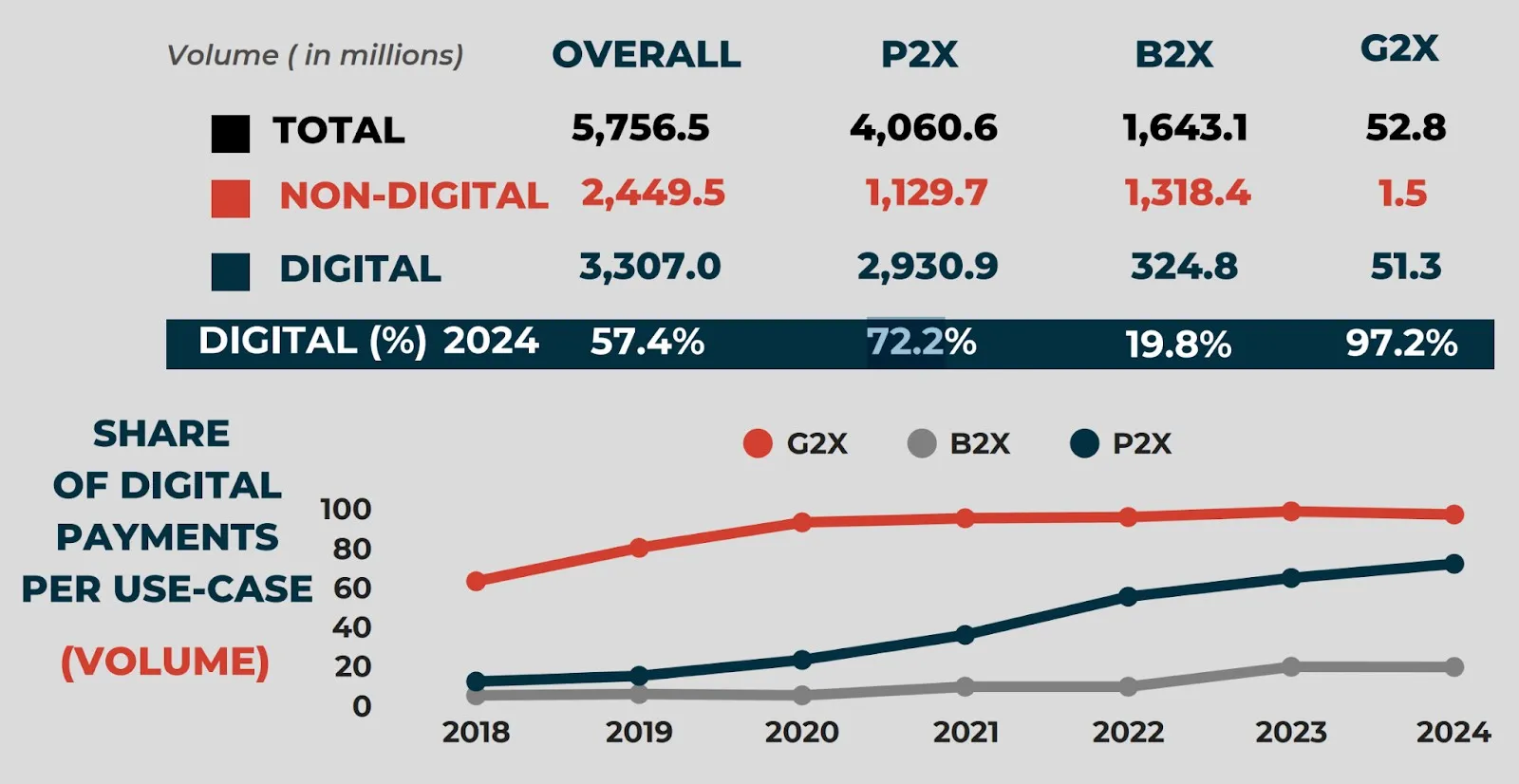

According to the report, the increase in digital payment adoption has been led by three key use cases: merchant payments, person-to-person (P2P) transfers, and business-to-business (B2B) supplier transactions. These accounted for 93.2% of the total volume, or 3.08 billion digital transactions in 2024.

Merchant payments were the largest contributor, increasing 29.1% year-on-year to 2.2 billion digital transactions. These made up 66.4% of the total digital transaction volume. P2P transfers followed, totaling 680.5 million transactions or 20.6% of volume. This marked a 34.7% growth from the year before. The report said this growth was driven by broader access to transaction accounts and resulted in P2P transfers seeing one of the highest jumps among all digital payment types.

B2B supplier payments increased from 160 million to 205 million digital transactions—an annual growth rate of 28.1%. “This reflects the impact of the BSP’s digitalization initiatives in the business sector,” the report stated.

InstaPay and PESONet usage expands rapidly

The use of fast payment channels like InstaPay and PESONet has grown considerably. “InstaPay also saw significant growth, with a 67.8% rise in transaction volume and 46.3% in value from 2023 to 2024, highlighting its popularity for fast, low-value P2P transfers,” the BSP stated.

Meanwhile, PESONet benefited from the expansion of its clearing cycles. “The expansion of PESONet transactions, supported by the addition of a third daily settlement cycle in July 2024, has further boosted digital supplier payments,” the report noted. These developments reflect consumer demand and payment infrastructure upgrades enabling faster, more flexible financial flows.

Government sector achieves nearly complete digitalization

Among the three main payment originators—Government (G2X), Businesses (B2X), and Persons (P2X)—the government sector achieved the highest level of digitalization. According to the BSP, 97.2% of government payments were processed digitally in terms of volume and value.

“Government disbursements are highly digitalized at 97.2%,” the report stated. This figure confirms the public sector’s continued leadership in adopting electronic payment mechanisms, especially for social transfers, wages, and supplier contracts.

Personal transactions see substantial gains in digital use

Personal payments (P2X) have made advances as well. The BSP found that 72.2% of P2X transactions were processed digitally by volume, while 80.4 % of their total value was digital, representing a 5.3% increase from 2023.

The BSP also recorded a decline in non-digital personal payments, which may signal a permanent behavioral shift. “A decrease in the volume of non-digital payments which could indicate a shifting preference to pay digitally,” the report stated.

Of the 5.8 billion retail transactions recorded in 2024, 70.5% originated from P2X payments. This made personal payments the dominant force in the retail space, not only in frequency but also in financial impact.

Source: BSP

Source: BSPBusiness transactions lag in volume but improve in value

While businesses still trail in digital volume, their contribution in terms of transaction value is rising. Just 19.8% of B2X transactions were digital by volume in 2024. However, they accounted for 38.6% of the total value, showing the growing impact of digital adoption in corporate finance.

“Business-to-business (B2B) payments accounted for 26.1%,” the BSP stated, referring to the share of business-to-business payments in the overall retail transaction mix. This indicates improved operational efficiency among firms using digital channels for supplier and vendor transactions.

Retail payments landscape still dominated by P2B and B2B

The BSP’s diagnostic study of retail payments showed that person-to-business (P2B) and business-to-business (B2B) payments together accounted for 83.5% of all transactions. “Person-to-business (P2B) payments made up 57.3%, reflecting increasing digital use for everyday expenses like merchant purchases, utilities, and loan repayments,” the BSP said.

“Notably, person-to-business (P2B) and business-to-business (B2B) payments together account for 83.5% of total retail payments, highlighting their strategic importance in driving payment system improvements,” the report added.

BSP’s vision: Digital by default, with consumer trust

Remolona said the central bank’s objective goes beyond improving statistics. “This is more than just a continuation of past gains. It is a reaffirmation of our collective vision, of a future where every Juan and Maria, no matter where they are in the archipelago, can access and benefit from secure, reliable, and convenient financial services.”

Remolona emphasized that innovation is a means to uplift people, especially the unbanked. “We recognize that innovation is not an end in itself, but a powerful means to reach people, especially the unbanked and underserved, with tools that uplift lives.”

Deputy Governor Mamerto Tangonan stressed the need for digital to become part of daily life. “We aim to move beyond first-time adoption to sustained, habitual use, where a person chooses to transact digitally not just once or occasionally, but consistently across different payments needs and platforms,” he said.

Tangonan added, “Our deeper challenge [is] to ensure that digital payments are not just adopted but be integrated into the daily lives of every Filipino.” Remolona concluded, “We envision a future where digital becomes the default, not only because it is mandated but because the end users see real value in its convenience, security and the feeling of empowerment.”

Regulatory focus: Safety, interoperability, and inclusion

The BSP underscored that trust and safety must accompany innovation. “Safety in payments, whether digital, physical or cross-border, is non-negotiable,” the report stated.

To this end, the BSP is building “a regulatory environment that is vigilant, agile and informed. One that works alongside innovation, not to stifle, but to guide its responsible use.” The ultimate goal is “a national retail payment system where one account is sufficient to meet all payment needs of a person in a secure and convenient manner.”

Cross-border, CBDC, QR, and direct debit are among key projects

Several initiatives launched or expanded in 2024 are aimed at accelerating progress. These include Project Nexus, which connects fast payment systems between the Philippines, India, Malaysia, Singapore, and Thailand. “This project aims to enhance cross-border payments by connecting the domestic instant payment systems of participating countries,” the BSP explained.

Project Agila, the BSP’s wholesale central bank digital currency (CBDC) pilot, tested institutional payments even when the RTGS system was down. Results will inform the BSP’s future CBDC roadmap.

QR Ph was also enhanced. “Users will now use InstaPay QR (with InstaPay logo) for P2P transfers, while the existing QR Ph code (red-blue-yellow logo) will continue for merchant payments,” the BSP stated.

Upcoming policies to improve affordability and oversight

The BSP is also advancing policy reforms. A draft circular proposes appointing designated managers for payment systems, while another mandates technical and governance requirements for clearing switch operators (CSOs).

In response to high transaction fees, the BSP is crafting policies to make digital payments more affordable and accessible. “High fees remain a barrier,” the BSP noted.

Circular No. 1195 addresses electronic fund transfer complaints, while Circular No. 1198 mandates that merchant payment service providers obtain licenses and adopt risk controls to protect consumer and merchant funds.

Digital growth continues as BSP pushes toward universal use

The BSP’s 2024 digital payments report highlights growing adoption across all user groups—from households to businesses and government agencies. With infrastructure improvements, regulatory safeguards, and a future-ready vision, the central bank aims to make digital payments not just widely available, but habitually used.

“We will continue to foster a digital finance ecosystem that is future-ready yet firmly grounded in trust, security, and consumer welfare. This means promoting innovation while maintaining the safeguards that protect users and ensure integrity across the system,” Remolona concluded.

Watch | Philippine Blockchain Week 2025: Web3 innovation goes from hype to use case

English (US) ·

English (US) ·