On Strategy's May 5 earnings call, Strategy CEO Phong Le said plainly that “we will sell Bitcoin when it is advantageous to the company,” with Saylor adding that Strategy would “probably sell some Bitcoin to fund a dividend just to inoculate the market.”

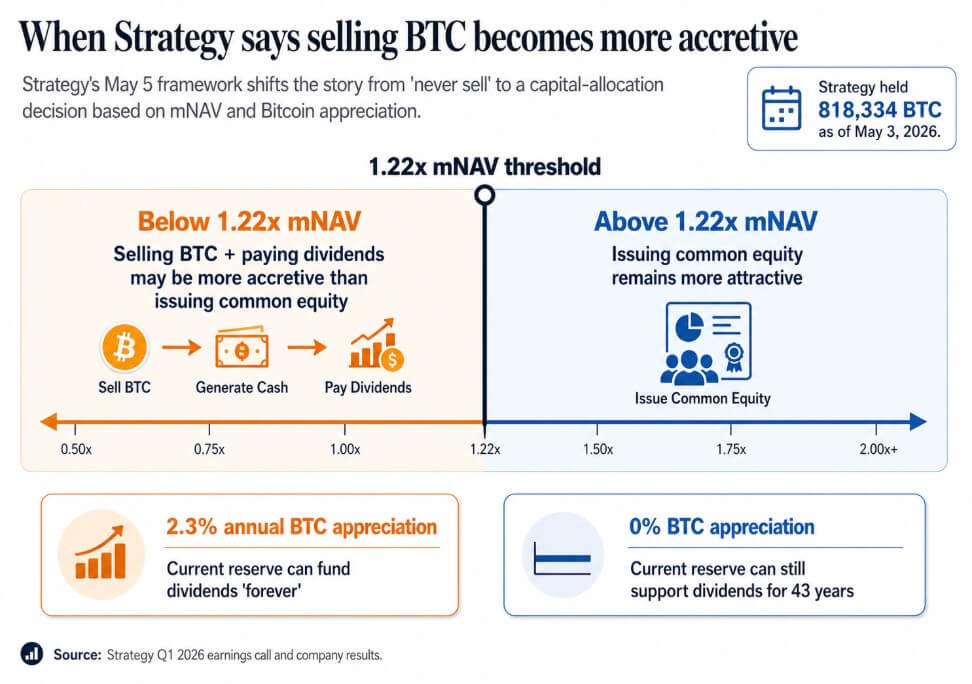

Strategy held 818,334 BTC as of May 3, up 22% year-to-date, with a market value of $64.14 billion.

What the May 5 call established was the public normalization of BTC sales as a corporate finance lever and the quantitative framework now sitting behind it

Below roughly 1.22x mNAV, management said selling BTC and paying dividends can be more accretive than issuing common equity. Saylor argued that if Bitcoin appreciates by just 2.3% annually, Strategy's current reserve can fund dividends “forever,” and if Bitcoin appreciates at zero, the reserve can still support dividends for 43 years.

The absolutist slogan gave way to a model in which companies that buy when accretive, issue equity when accretive, issue preferreds when accretive, and sell BTC when accretive are leveraged treasury-and-credit vehicles.

Investors originally bought these companies as Bitcoin proxies built on scarcity and permanence. The 1.22x mNAV threshold and the 2.3% breakeven rate are a more honest version of that pitch, and a more complicated one.

An infographic outlines Strategy's 1.22x mNAV threshold, showing when selling Bitcoin to fund dividends becomes more accretive than issuing common equity.

An infographic outlines Strategy's 1.22x mNAV threshold, showing when selling Bitcoin to fund dividends becomes more accretive than issuing common equity.When Bitcoin becomes liquidity

Sequans reported first-quarter revenue down 24.8% year over year to $6.1 million, alongside a $50.5 million operating loss. The first quarter included $11.7 million in realized net losses from Bitcoin sales, with proceeds primarily allocated to convertible debt redemption and an ADS buyback program.

As of Mar. 31, it held 1,514 BTC, with 1,217 BTC serving as collateral against $66.2 million of convertible debt. By Apr. 30, it held 1,114 BTC, with 817 BTC serving as collateral against $35.9 million of debt due by June 1.

This follows the same pattern as in November 2025, when Sequans sold 970 BTC to redeem 50% of its convertible debt, reducing that obligation from $189 million to $94.5 million.

Over two quarters, when revenue falls and debt comes due, Bitcoin becomes operational liquidity. The pledged collateral structure commits BTC that the company nominally holds as collateral against obligations before any sale decision.

Sequans operates at a different scale from Strategy, with a weaker operating business behind its treasury position. When BTC has to fund immediate debt service, inventory logic takes over.

MARA applied the same logic in March on a larger scale, selling 15,133 BTC for approximately $1.1 billion and using the proceeds to repurchase convertible notes, thereby cutting outstanding convertible indebtedness by about 30% and capturing roughly $88.1 million in value.

MARA packaged the move as balance sheet optimization driven by debt structure and financing conditions, establishing that BTC sales can arrive as capital allocation decisions independent of Bitcoin conviction, and that the relevant question for treasury companies is under what conditions selling becomes the highest-return move.

| Strategy | Publicly normalized potential BTC sales | Held 818,334 BTC as of May 3 | Could sell BTC to fund dividends if more accretive than issuing equity | BTC is now part of the corporate-finance toolkit, not just a reserve asset |

| Sequans | Sold BTC while under operating and debt pressure | BTC holdings fell from 1,514 on Mar. 31 to 1,114 on Apr. 30 | Debt redemption and ADS buyback | BTC becomes liquidity when revenue weakens and debt matures |

| MARA | Sold BTC for liability management | Sold 15,133 BTC for about $1.1B | Repurchase convertible notes, cut debt by about 30% | BTC sales can be framed as balance-sheet optimization, not just distress |

What the shift decides

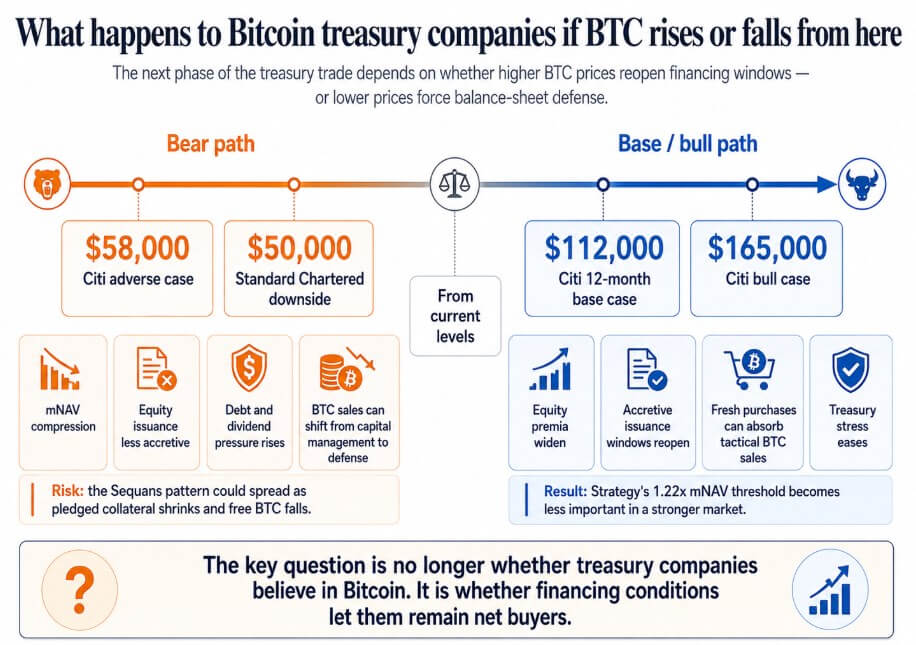

If Bitcoin recovers toward Citi's 12-month base-case target of $112,000 or its bull case of $165,000, equity premia across treasury companies widen, accretive issuance windows reopen, and larger fresh purchases absorb tactical BTC sales.

Strategy's 1.22x mNAV threshold fades into a technical detail, and Sequans-type firms that faced debt stress through a weak Bitcoin market resolve their obligations and hold unrestricted BTC heading into the next cycle.

If Bitcoin moves toward Citi's $58,000 adverse case, which Standard Chartered has flagged as a potential path to $50,000, companies trading near or below NAV lose accretive access to equity markets.

In this scenario, preferred dividend obligations compound, and BTC sales move from capital management to balance sheet defense.

The Sequans pattern could spread to any treasury company that combined thin operating revenue with BTC-backed borrowing, where selling Bitcoin to service debt while pledged collateral shrinks the free float becomes the only available response.

At that point, the corporate Bitcoin bid turns into a cycle in which falling prices trigger more selling, pushing prices lower.

An infographic maps two Bitcoin price paths for treasury companies, contrasting bear case balance-sheet stress at $50,000–$58,000 against bull-case financing relief above $112,000.

An infographic maps two Bitcoin price paths for treasury companies, contrasting bear case balance-sheet stress at $50,000–$58,000 against bull-case financing relief above $112,000.The corporate Bitcoin treasury trade rested on the promise of permanent accumulation, which made these companies legible to investors as proxies for Bitcoin.

Once selling becomes an acknowledged tool inside the model, investors have to price in debt maturities, collateral requirements, dividend obligations, and the mNAV thresholds at which management may decide selling outperforms issuing equity.

Saylor's 2.3% appreciation breakeven and 1.22x mNAV threshold are more honest. The next phase of the Bitcoin treasury trade will be decided as much by financing conditions as by Bitcoin conviction.

English (US) ·

English (US) ·