On May 28, Aave Labs announced that its UK subsidiaries Push Labs Ltd. and Push Virtual Assets Ltd. received FCA registration as cryptoasset exchange providers, layered on top of the group's existing Electronic Money Institution authorization.

Combined with the MiCAR CASP license that Push Virtual Assets Ireland Limited secured from the Central Bank of Ireland in November 2025, Aave now operates under a dual-permission framework covering both the UK and the EEA.

The licensing stack clears the path for zero-fee fiat-to-stablecoin on and off-ramps and, according to Stani Kulechov, “next-generation, zero-fee on-chain consumer financial products.”

Aave's competitive edge comes from its position as the largest on-chain credit market, with nearly $14 billion in total value locked (TVL) and $10.7 billion in outstanding borrowings, according to DefiLlama.

Adding a regulated consumer payments layer to that stack would look like a random expansion, unless it feeds directly into Aave's lending protocol, which is exactly what Push is designed to do.

What makes Push worth examining more closely is that it is being built as the regulated front door to Aave's lending protocol, the channel through which bank accounts convert to stablecoins and stablecoins flow into GHO, savings, and borrowing on Aave.

Why payments have historically failed Aave

Marc Zeller's February governance audit tallied Aave Labs' total capitalization at roughly $86 million, with $16.2 million from the 2017 EthLend ICO, $32.5 million from venture rounds, $31.9 million in direct DAO payments, and approximately $5.5 million in swap fees he characterized as unapproved.

His framework applied three questions to that figure: what did Labs deliver, what did it cost, and what was the return?

The audit concluded that non-core products had not shown cost-per-outcome discipline commensurate with that funding. Zeller specifically called out Horizon, Aave's RWA marketplace, for a spending-to-revenue ratio of approximately 24:1.

The broader indictment was that Labs had captured brand-adjacent revenue streams, such as swap fees routed to a Labs-controlled wallet rather than the DAO treasury, while expanding its product scope with no measurable impact on the protocol.

That critique shaped the AIP 469 vote, which passed with roughly 75% of participating tokens. It established the “Aave Will Win” framework, consisting of routing to the DAO treasury 100% of revenue from all Aave-branded products, including the frontend app, Aave Card, Aave Pro, swaps, and future consumer products.

In exchange, Aave Labs received a $25 million stablecoin grant and 75,000 AAVE vesting over 48 months.

Zeller's Aave Chan Initiative cast 166,200 tokens against, the largest single dissenting vote, before announcing ACI would wind down entirely by July.

| 2017 EthLend ICO | $16.2M | Early capitalization base |

| Venture rounds | $32.5M | Private funding behind Labs growth |

| Direct DAO payments | $31.9M | DAO-funded product accountability |

| Swap fees characterized as unapproved | ~$5.5M | Core dispute over value capture |

| Total cited by Zeller | ~$86M | Baseline for “what did Labs deliver?” critique |

| Aave Will Win funding | $25M + 75,000 AAVE | New test: funding tied to DAO revenue routing |

| Product-revenue routing | 100% to DAO treasury | Why Push is judged differently from prior side quests |

The governance fight changed the accountability structure for non-core product development, directly shaping Push's trajectory.

Labs can no longer capture payments-adjacent revenue independently, and any flow Push generates falls under the DAO revenue framework. That moves the incentive structure from “Labs builds a consumer fintech” to “Labs builds a distribution layer whose commercial output belongs to AAVE holders.”

Payments as a funnel and lending as the business

Kulechov's January framework post showed that most Aave lending is still concentrated around ETH, BTC, and leverage-driven looping strategies tied to crypto market cycles.

GHO's circulating supply sits near 584 million tokens, making it pale in comparison to USDT's share of the $188 billion stablecoin market and USDC's $76 billion.

Aave's addressable stablecoin opportunity is orders of magnitude larger than its current penetration, and the disconnect comes down to getting regular capital into the protocol without routing it through crypto-native infrastructure.

Aave already generates over $633 million in annualized fees and $81 million in annualized revenue. The missing layer is a regulated, zero-fee ramp from bank accounts to stablecoins, and Push is built to supply it.

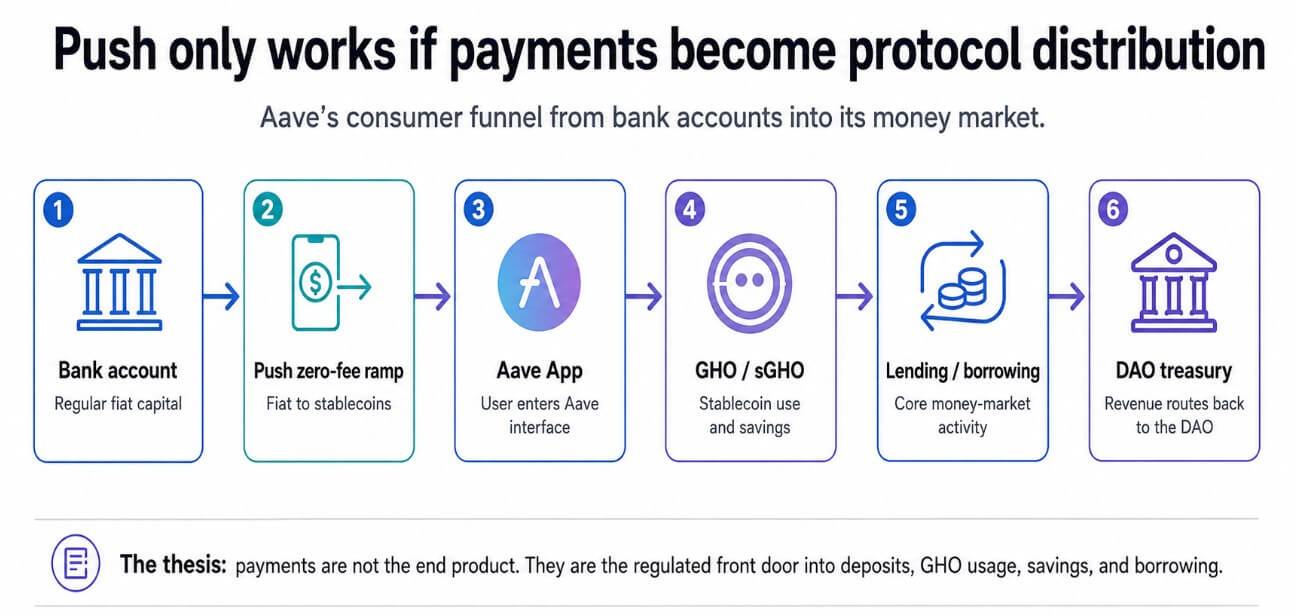

The user journey Push enables runs from a bank account to a zero-fee stablecoin ramp to the Aave App to GHO or sGHO savings to lending and borrowing. A generic payments product monetizes through spreads, interchange, or subscription fees.

A six-step flowchart shows how Aave's Push layer channels users from bank accounts into its money market, routing revenue to the DAO.

A six-step flowchart shows how Aave's Push layer channels users from bank accounts into its money market, routing revenue to the DAO.Push's revenue comes from users moving deeper into Aave's money market, depositing stablecoins, minting GHO, holding sGHO, and borrowing against collateral. The deeper users go, the more protocol revenue accrues to the DAO.

The Irish MiCAR license already supports zero-fee euro-to-stablecoin conversion, and the UK FCA registrations extend that infrastructure to a second major regulated market, with EEA passporting rights already in place from Ireland.

Coinbase, MoonPay, Ramp, and Revolut all compete for the same fiat-to-crypto conversion flow, and that market is inherently low-margin.

Push's structural advantage lies in its non-custodial design, combined with a regulated presence in two major markets, which removes one of the most friction-heavy steps in converting a regular consumer into an Aave depositor.

If Push retains even 2.5% of its converted stablecoin flow into Aave deposits, roughly $500 million at scale, it reaches parity with GHO's current market cap. It creates an acquisition channel that operates entirely outside crypto-native leverage cycles.

What has to hold

The bear case is identical to every prior Aave expansion Zeller warned about, consisting of Push becoming a regulated payments layer with high ramp volume and low protocol conversion.

If Push users convert fiat to stablecoins and withdraw to external wallets or competing platforms, Push becomes expensive infrastructure generating no Aave-native value.

The FCA and MiCAR licenses enable legal operation, and converting that permission into deposit growth requires a consumer product that pulls users away from Revolut, Monzo, and Coinbase on product quality.

Revolut, Monzo, and Coinbase's UK entity have occupied this market for years with established compliance functions, brand recognition, and integrated product suites.

The UK's broader crypto licensing regime also introduces timing risk, as the FCA has confirmed that current Money Laundering Regulation registrations will not automatically convert into authorization under the forthcoming FSMA-based framework, set to take effect in October 2027.

Push's current registration clears the path for launch but does not guarantee a frictionless transition into the stricter regime.

And the governance structure that makes Push's revenue alignment credible depends on Aave Labs maintaining enough internal cohesion to execute a consumer product roadmap.

Aave's money market is deep enough that Push only has to move a fraction of consumer stablecoin flow into Aave deposits to justify its existence.

| Bull case: money-market funnel | Push users convert fiat, then retain funds in Aave deposits, GHO, or sGHO | Deposit retention, GHO supply growth, sGHO adoption | Payments strengthens Aave’s lending moat |

| Base case: useful ramp | Push gets adoption, but much of the flow exits to external wallets or venues | Ramp volume vs Aave deposit conversion | Helpful infrastructure, but not a core growth engine |

| Bear case: side quest returns | High compliance/product cost, weak protocol conversion | Cost per retained dollar, protocol revenue uplift | Zeller’s critique is validated |

| Regulatory risk case | UK FSMA transition or EEA compliance limits product design | Approval status, launch scope, product restrictions | Licensing win becomes execution risk |

| Governance risk case | DAO/Labs alignment frays over costs, revenue, or product scope | DAO revenue share, reporting cadence, renewal votes | AWW framework faces its first major stress test |

If it does, payments become Aave's most important acquisition channel, and Zeller's cost-per-outcome framework finally gets a product that passes it.

If Push produces ramp volume without protocol conversion, the framework applies in reverse: another product layer, another governance fight, the same unresolved question about what Aave Labs builds that actually strengthens the money market versus what it builds for other reasons.

The Aave Will Win framework was designed to make that distinction testable, and Push is the first product that runs the experiment in a regulated consumer market.

English (US) ·

English (US) ·